The road ahead

The Carbon Border Adjustment Mechanism (CBAM) represents a significant policy initiative by the European Union (EU) to limit carbon emissions and address climate change. The CBAM aims to level the playing field for EU producers by imposing a carbon cost on imports of certain goods from outside the EU, thereby preventing ‘carbon leakage’ – the transfer of production to countries with looser emission restrictions. In this article, Thanh Tran and Nora Zhang of TERAO set out what businesses need to do to prepare for the CBAM.

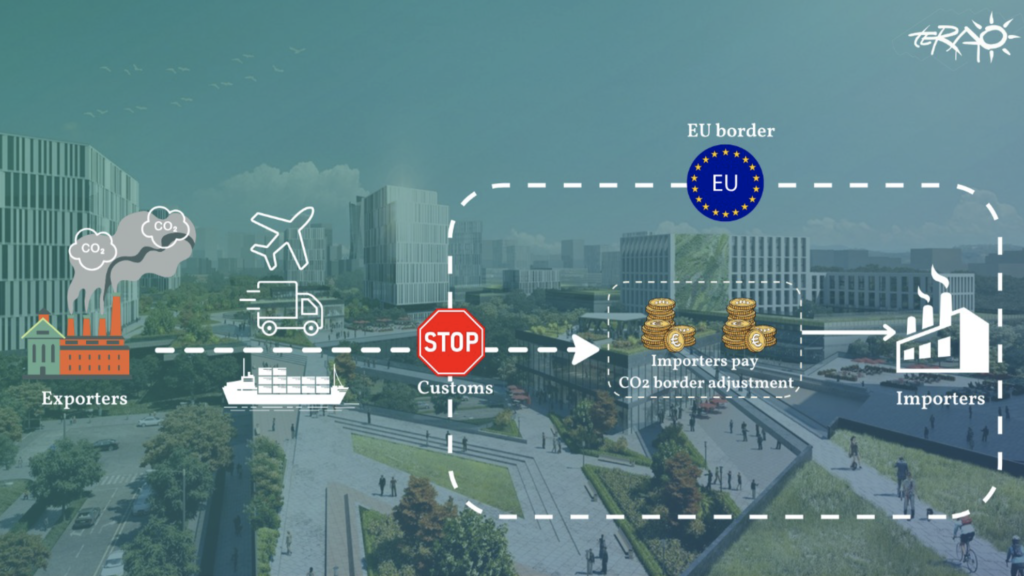

CBAM Mechanism

Set to be fully implemented in 2026, the EU’s CBAM is designed to ensure that imported goods are subject to the same carbon pricing as products produced in the EU. It will initially target sectors that are particularly carbon intensive and at risk of carbon leakage. These sectors include iron and steel, aluminium, cement, fertilisers, electricity and hydrogen. Companies in these sectors must now account for the carbon emissions embedded in their products, aligning their practices with EU standards. The mechanism will expand gradually, potentially encompassing more than half of the emissions covered by the EU Emissions Trading System (ETS) by 2034.

The CBAM affects EU importers that import goods from the targeted sectors and non-EU producers exporting these goods to the EU. Companies in sectors such as automotive manufacturing, aerospace and capital goods, which rely on materials like steel and aluminium, are particularly impacted. They must adapt to the new regulations and potentially face big choices, such as finding suppliers with lower carbon emissions or investing in cleaner production methods. They will also need to plan for higher costs due to the need to buy CBAM certificates. Companies must also ensure that they report emissions correctly and buy the correct number of certificates.

The mechanism requires EU importers to purchase CBAM certificates that reflect the carbon price of EU ETS allowances. Importers can deduct any carbon costs already paid in the country of origin from their CBAM charge. The mechanism is designed to be compliant with World Trade Organization (WTO) rules and will replace the free allocation of EU ETS allowances currently provided to EU industries.

The transitional phase of the CBAM began on 1st October 2023 and will run until 31st December 2025. During this time, businesses must report the carbon emissions of their goods. It aims to help importers and producers prepare for the full implementation of the CBAM in 2026. From then on, reporting becomes mandatory and importers must purchase CBAM certificates. Non-compliance could lead to penalties, delayed customs clearance and negative records. A negative record has several implications: future shipments may be subject to more stringent inspections and delays, and additional fees or fines may be applied for continued non-compliance. A history of non-compliance might damage a company’s reputation with customs authorities and business partners; in severe cases, persistent non-compliance may result in legal action or restrictions on import and export activities.

CBAM Timeline

The calculation of CBAM charges involves determining the embedded emissions in imported goods. Initially, one must identify the goods subject to the CBAM, which typically include high-carbon products. The next step is to gather the necessary emissions data, which can be either estimated or actual data from suppliers using default values provided by the EU. If actual data is unavailable, emissions can be estimated by multiplying the weight of the imported goods (in tonnes) by the emissions factor, which represents emissions per tonne. This calculation is important for companies to comply with EU regulations and prepare for the financial period starting in 2026, when they need to purchase CBAM certificates corresponding to the carbon cost of imports. The price of CBAM certificates is pegged to the weekly average auction price of EU ETS allowances. Importers must declare these emissions and submit the corresponding number of certificates annually.

| Emissions = Weight of imported goods (in tonnes) x Emissions per tonne |

The CBAM aims to level the playing field and reduce carbon leakage, but it presents several financial risks and challenges for European businesses operating in China. These businesses need to adapt their strategies to manage the impact of the CBAM effectively.

- Increased costs: European businesses importing goods from China will face increased costs due to the need to purchase CBAM certificates. The cost of these certificates will be based on the carbon emissions embedded in the imported goods, which could vary significantly depending on the sectors and the carbon intensity of the production process.

- Supply chain disruption: The introduction of the CBAM may lead to supply chain disruptions as businesses adjust to the new requirements. Companies may need to look for alternative suppliers or invest in reducing carbon emissions in their supply chains to mitigate the financial impact.

- Market access risks: Non-EU suppliers, including those in China, may face the risk of losing market access if they cannot comply with CBAM requirements. This could lead to a reduction in the competitiveness of Chinese exports to the EU, affecting European businesses that rely on these imports.

- Regulation compliance costs: Businesses will incur additional costs related to compliance with CBAM regulations, including monitoring, reporting and verifying carbon emissions. These compliance could be significant, especially for companies with complex supply chains.

To comply with the CBAM, companies need to establish robust systems to monitor and report greenhouse gas emissions across their supply chains. This includes both direct and indirect emissions embedded in imported goods. Non-compliance could lead to increased carbon tax costs and reduced competitiveness in the EU market.

The CBAM is a bold step towards a greener economy, encouraging global industries to align with the EU’s ambitious climate goals. Companies must proactively engage with the CBAM requirements to avoid potential fines and loss of market share. It is time for businesses to invest in sustainable practices and prepare for a future in which environmental accountability is not only encouraged but enforced.

Thanh Tran is marketing manager at TERAO. Nora Zhang is the company’s China sales manager.

TERAO is a French building sustainability consultancy with three decades of experience. Since 2008, the company has extended its presence in Asia through five primary hubs (China, Vietnam, Thailand, Singapore and Malaysia), with plans for further expansion in the rest of Southeast Asia, India, the Middle East and beyond. Specialising in reducing the environmental impact of buildings, TERAO offers expertise for both new construction and existing assets across diverse sectors and building types, including hospitality, manufacturing, retail and healthcare.

[1] Carbon Border Adjustment Mechanism, European Commission, 4th November 2024, viewed 4th December 2024, <https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en>

Recent Comments